Pensions – Part 1

Currently the UK Government is discussing a proposal that would see the state pension age rise to 75. These ideas from the Tory think-tank the Centre for Social Justice (CSJ) have been branded “chilling and immoral” by former pensions minister Ros Altmann. The UK pension age is already set to increase to 67 by 2028 and to 68 by 2046 and if these changes are implemented it would see the retirement age rise to 70 by 2028 and 75 by 2035.

Currently the UK Government is discussing a proposal that would see the state pension age rise to 75. These ideas from the Tory think-tank the Centre for Social Justice (CSJ) have been branded “chilling and immoral” by former pensions minister Ros Altmann. The UK pension age is already set to increase to 67 by 2028 and to 68 by 2046 and if these changes are implemented it would see the retirement age rise to 70 by 2028 and 75 by 2035.

In the UK you can find your expected date you ‘might expect’ to receive your state pension under CURRENT rules. However, as the above suggests this is a movable feast, or since we are also likely to receive less in real terms a movable snack!

Is this a betrayal of hard-working people who had planned and saved for their retirements? On the surface it looks like it, however we are living longer than was expected when the original calculations were made and thus the ‘pension pot’ we have contributed to has to stretch to cover these extra years so something has to give. If it’s you who is expected to ‘give’ more, work longer and receive less it will probably feel rather unfair.

Is this a betrayal of hard-working people who had planned and saved for their retirements? On the surface it looks like it, however we are living longer than was expected when the original calculations were made and thus the ‘pension pot’ we have contributed to has to stretch to cover these extra years so something has to give. If it’s you who is expected to ‘give’ more, work longer and receive less it will probably feel rather unfair.

In the UK keeping the working population employed until their mid-70s may help to boost the economy by £182 billion a year but some of this may well be used up by the “farcical prospect” that 74-year-olds who could not find work would have to apply for unemployment benefits. More than a million over-50s want to work but can’t find a job in part due to age discrimination. Increasing support with retraining programmes and employer incentives as a first priority MAY help minimise the increase in the state pension age.

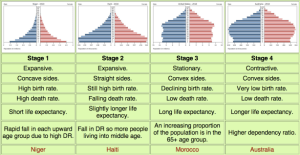

A growing challenge for many nations is their ageing population. As birth rates drop and life expectancy increases an ever-larger portion of the population is elderly leaving fewer workers to contribute taxes for each retired person’s pension. In most developed countries government and public sector pensions could potentially be a drag on their economies unless pension systems are reformed with increased retirement age or tax increases. Two exceptions are Australia and Canada where the pension system is forecast to be solvent for the foreseeable future. The Canadians increased the annual payments by some 70% in 1998. This is in contrast to the recent trend of states and businesses in the United States to purposely under-fund their pension schemes in order to push the costs onto the federal government. For example, in 2009, most states unfunded pension liabilities exceeding all reported state debt. Bradley Belt, former executive director of the PBGC (the Pension Benefit Guaranty Corporation, the federal agency that insures private-sector defined-benefit pension plans in the event of bankruptcy), testified before a Congressional hearing in October 2004, “I am particularly concerned with the temptation, and indeed, growing tendency, to use the pension insurance fund as a means to obtain an interest-free and risk-free loan to enable companies to restructure. Unfortunately, the current calculation appears to be that shifting pension liabilities onto other premium payers or potentially taxpayers is the path of least resistance rather than a last resort. “The post-2007 credit crunch created further challenge. Total funding of the US’s 100 largest corporate pension plans fell by $303bn in 2008, going from a $86bn surplus at the end of 2007 to a $217bn deficit at the end of 2008.

A growing challenge for many nations is their ageing population. As birth rates drop and life expectancy increases an ever-larger portion of the population is elderly leaving fewer workers to contribute taxes for each retired person’s pension. In most developed countries government and public sector pensions could potentially be a drag on their economies unless pension systems are reformed with increased retirement age or tax increases. Two exceptions are Australia and Canada where the pension system is forecast to be solvent for the foreseeable future. The Canadians increased the annual payments by some 70% in 1998. This is in contrast to the recent trend of states and businesses in the United States to purposely under-fund their pension schemes in order to push the costs onto the federal government. For example, in 2009, most states unfunded pension liabilities exceeding all reported state debt. Bradley Belt, former executive director of the PBGC (the Pension Benefit Guaranty Corporation, the federal agency that insures private-sector defined-benefit pension plans in the event of bankruptcy), testified before a Congressional hearing in October 2004, “I am particularly concerned with the temptation, and indeed, growing tendency, to use the pension insurance fund as a means to obtain an interest-free and risk-free loan to enable companies to restructure. Unfortunately, the current calculation appears to be that shifting pension liabilities onto other premium payers or potentially taxpayers is the path of least resistance rather than a last resort. “The post-2007 credit crunch created further challenge. Total funding of the US’s 100 largest corporate pension plans fell by $303bn in 2008, going from a $86bn surplus at the end of 2007 to a $217bn deficit at the end of 2008.

Behaviourally it is difficult for most people to save enough on their own volition to finance their retirement, which argues for some form of ‘automatic-enrolment’ such as with the UK’s Pensions Act of 2008 whereby every employer must put their qualifying employees into a pension scheme and where appropriate also pay contributions.

In their book ‘The 100 year Life’ Lynda Gratton and Andrew Scott discuss the conundrum and how we as a society might manage this. They conclude that the level of savings required to support a lengthy period of retirement at the end of a 100-year life is unachievable even assuming a 3% real rate of return on investments and a pension contribution of 17% of income for an individual born in 1971 to support a replacement income of 50% in retirement. However work done by Schroders (Lessons learned in DC from around the world, 2013) suggests this is an overly bleak perspective and also that the issue is more complex. The assessment of an appropriate replacement rate of income from defined contribution pensions depends on the level of the state pension and also varies according to levels of income in employment: those on low incomes need a much higher replacement rate. Schroders suggest later and more flexible retirement dates are inevitable and are already taking effect in many countries, but this trend need not go as far as having an expectation of working into ones 80s. Schroders somewhat less pessimistic conclusion is that a combination of 15% contributions, a 3% real rate of return and a modest increase in retirement age is the minimum necessary to achieve an adequate standard of living in retirement. Indeed, the generally admired compulsory Australian pension system is currently based on eventually reaching 12% contributions.

MoneySavingExpert.com suggests as a rule of thumb for individuals that you take the age you start your pension and halve it. Put this % of your pre-tax salary aside each year until you retire. Make sure you include your employer’s contribution in that percentage. So, someone starting aged 32 should contribute 16% of their salary for the rest of their working life.

Certainly paying pensions to the retired for 30 – 40 years with the current system is impossible and many governments have made it mandatory that employees and employers have pension plans and contributions. These will have to start earlier, be a bigger proportion of income and be paid out much later in life.

Pension age should rise to 75, Tory think tank report says

Former UK pensions minister Ros Altmann suggests that proposals currently under consideration by the UK government would also likely shorten the life expectancy of those in disadvantaged parts of Britain and that she had rarely seen a proposal “with the potential to do such damage”. “The better-off, whose employment does not usually entail physical labour, might hope to live well into their 80s with good health,” she said. “But for people burned out by tough manual work, who tend to have poorer housing, diets, access to healthcare and are at greater risk of ill-health and frailty, death comes much sooner. This is already a grave injustice in our society. Driving up the pension age even further makes it worse – particularly for those groups who are statistically more likely to die in their late 60s or early 70s, who will suddenly see the finishing line pushed so far into the distance that it becomes meaningless.”

Interestingly the view of Lynda Gratton and Andrew Scott in their book ‘The 100 year Life’ is that work will change dramatically with AI (artificial intelligence) and mechanisation with robotics etc. stripping out much of what we do now. A machine will likely be able to read legal documents and suggest legally robust solutions, analyse medical data from across the world and plan treatment regimes based on this evidence even better than a doctor with 30-40 years’ experience – especially with rare conditions where the data and knowledge is not available locally. Autonomous vehicles built by robots and learning from each other in real-time may reduce accidents and thus the need for roving mechanics as well as emergency room doctors. Who knows what jobs our grandchildren will be doing, however almost certainly their work will look very different from ours and as my daughter retorted to the question “What do you want to be when you grow up?” – “I don’t know, my job might not have been invented yet!”

Q. Have you calculated how much you need to live on in retirement?

Q. Are you going to have to work longer, pay in more pension contributions and receive less?

Q. Is your TOYL going to be expensive or are you content with a less luxurious lifestyle?

Let me know your feelings, ideas and comments!

[…] Pensions: https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ […]

LikeLike

[…] Income (More at https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ and […]

LikeLike

[…] Income (More at https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ and […]

LikeLike

[…] Pensions: https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ […]

LikeLike

[…] Pensions: https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ […]

LikeLike

[…] Pensions – Part 1 […]

LikeLike

[…] Pensions: https://itsthetimeofyourlife.com/2019/08/26/pensions-part-1/ […]

LikeLike

[…] Pension – Part 1 […]

LikeLike